�

Working Paper No. 05-01 Essential elements of a modern monetary economy with applications to social security privatisation and the intergenerational debate

William Mitchell and Warren Mosler[1]

February 2005�

Centre of Full Employment and Equity

The University of Newcastle, Callaghan NSW 2308, Australia

Home Page: http://e1.newcastle.edu.au/coffee/

Email: [email protected]1.�Introduction

There is considerable disparity among Post Keynesian conceptions of how a discourse in macroeconomics should proceed. This paper outlines a schematic framework grounded in functional finance which we argue defines the essential elements of a modern monetary economy (defined in the context of an economy with a sovereign government issuing a fiat currency with flexible exchange rates).

The paper also discusses two applications that are currently in vogue in the public policy debate: (a) the proposal by the US Government to 'privatise' its social security (pension) system; and (b) the proposal of the Australian Federal Government that it needs to run budget surpluses now to 'provide' for the increasing fiscal needs of the ageing population. These applications provide excellent case studies that expose the failings of current macroeconomic reasoning on both the orthodox (neo-liberal) side and also among many so-called Post Keynesians.

In recent years, there has been a substantial debate in the US concerning the 'viability' of their pension scheme and this has manifest in the US President's proposal in his February 2005 'State of the Union' speech to privatise the system because in his own words �By 2018, Social Security will owe more in annual benefits than the revenues it takes in, and when today's young workers begin to retire in 2042, the system will be exhausted and bankrupt" (State of Union, 2005).

The social security privatisation is being driven, in part, by philosophical notions of what constitutes 'individual freedom' and the US President's concept of an 'ownership society'. The aim is to broaden this concept of independence and private ownership to the traditional responsibilities of government - social security, broad access health care and education. The belief is that only if these areas of life are 'privately owned' can freedom being truly said to manifest. This paper expresses no opinion on this 'political question'. Rather, we argue that the economic basis of the agenda � that government bankruptcy is inevitable given the current demographic trends - is not applicable to a modern fiat currency using economy. Further, the amount of 'wealth' held in the US social security trust fund is largely irrelevant to its viability. The only relevant issue that confronts the US policy makers are the political choices that will have to be taken which will determine the distribution of available real resources across the population. This is a choice being made everyday by societies and governments in a more or less smooth fashion. But however difficult these 'choices' might become in the future there is never a risk of government insolvency.

The US social security privatisation debate has echoes in Australia with the claims that a number of federal programs (such as health and social security) are sensitive to demographic factors and with population ageing, the budget 'blow out' will be unsustainable (Commonwealth Treasury, 2002: 4). While government and business have supported the continued pursuit of budget surpluses for many reasons, the theme underlying the pro-surplus rhetoric has become centred on these so-called intergenerational issues. To cement this persuasion into an 'analytical' framework, the Australian government published its long awaited Intergenerational Report (IGR) as Budget Paper No.5, one of the 2002-03 Budget documents (Commonwealth Treasury, 2002, hereafter IGR).

The IGR summarised the implications of the analysis as follows: (a) the budget cannot be allowed to reach the projected level because the increasing public debt would push interest rates up and 'crowd out' productive private investment; (b) increasing debt will also impose higher future taxation burdens for our children which will reduce their future disposable incomes and erode work incentives; (c) the private sector must save more; (d) the economy must produce more jobs and people must work longer to accumulate more funds to finance their own retirements; and (e) higher levels of immigration are required to reverse the ageing bias in the population.

We show in this paper that the basic monetary assumptions of the IGR are without any application once there is a complete understanding of the dynamics of a floating exchange rate policy in regard to the government of issue. Overall, there has been a failure to criticise the basic monetary premises underlying the IGR. We show that Federal spending is not inherently financially constrained and does not have to be facilitated via prior taxation or debt-issuance. We also refute the claim that budget deficits cause higher interest rates, lower levels of capital formation and diminished rates of economic growth. These misconceptions together lead to the nonsensical claim that by running surpluses now the Government will be better able (because it has 'more funds stored away') to cope with future spending demands.

We argue that in fact, the pursuit of budget surpluses as a means of accumulating 'future public spending capacity' is not only without standing but also likely to undermine the capacity of the economy to provide the resources that may be necessary in the future to provide real goods and services of a particular composition desirable to an ageing population. We argue that by achieving and maintaining full employment via appropriate levels of net spending (deficits) the Government would be providing the best basis for growth in real goods and services in the future. We conclude that in a fully employed economy, the intergenerational spending decisions come down to political choices sometimes constrained by real resource availability, but in no case constrained by monetary issues, either now or in the future.

We thus argue that the social security privatisation debate in the US and the intergenerational debate in Australia are being driven by the same macroeconomic misunderstandings and dissipate into (interesting) political debates once the so-called economic issues are shown to be erroneous. We thus challenge the validity of these public debates at their most elemental level and conclude that the mainstream position is misguided at best.

2.�The rudiments of monetary macroeconomics

The essential operations of the macroeconomic system are often well explained in an introductory macroeconomics course. Sadly, the rudiments are quickly obfuscated as professors seek to replace them with increasingly difficult formal conceptions that distort the understanding students have of actual monetary economies. In this section, the rudiments of macroeconomics are restated to ensure that a firm understanding of the options and responsibilities for modern governments is achieved (see Mitchell and Mosler, 2002).

2.1 Modern monetary economies use fiat currencies

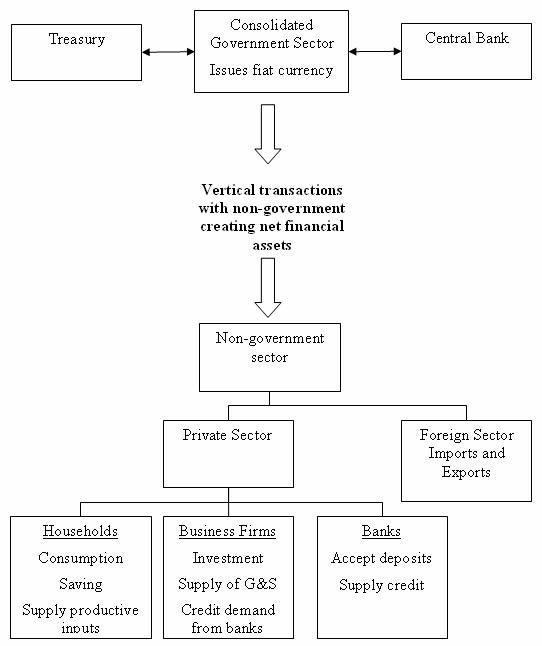

We begin our understanding of macroeconomics by outlining the importance of government in a modern monetary economy as outlined in Wray (1998) and Mitchell and Mosler (2002). Modern monetary economies use fiat currencies, such that the unit of account (including the monetary unit defined by the government) is convertible only into itself and not legally convertible by government into gold as it was under the gold standard, or any real good or service. In other words, we are talking about a flexible exchange rate policy, as contrasted with a fixed exchange rate policy. The definition of the currency of issue is made operational by acknowledging that it is the only unit which is acceptable for payment of taxes and other financial demands of the government of issue. The use of fiat currency presents the Government with a range of options it would not otherwise have, for example, under a fixed exchange rate policy, such as a commodity money system. Most relevant is that the government of issue (and its designated agents) is the single supplier of the currency units it demands for payment of taxes.

In Figure 1, we see the essential structural relations between the government and non-government sectors. First, there is no real significance in separating Treasury and Central Bank operations. While 'within government' transactions occur, they are of no importance to understanding the vertical relationship between the consolidated government sector (treasury and central bank) and the non-government sector. Second, extending the model to distinguish the foreign sector makes no fundamental difference to the analysis and as such the private domestic and foreign sectors can be consolidated into the non-government sector without loss of analytical insight.

As a matter of accounting between the sectors, a government budget deficit adds net financial assets (adding to non government savings) and a budget surplus has the opposite effect. The last point requires further explanation as it is crucial to understanding the basis of modern money macroeconomics.

While typically obfuscated in standard textbook treatments, at the heart of national income accounting is an identity - the government deficit (surplus) equals the non-government surplus (deficit). In aggregate, there can be no net savings of financial assets of the non-government sector without cumulative government deficit spending. In other words, the only entity that can provide the non-government sector with net financial assets (net savings) and thereby simultaneously accommodate any net desire to save and thus eliminate unemployment is the government. It does this by net spending. Additionally, and contrary to mainstream rhetoric, the systematic pursuit of government budget surpluses is necessarily manifested as systematic declines in private sector savings.

A simple example helps reinforce these points. Suppose the economy is populated by two people, one being government and the other deemed to be the private sector (see Nugent, 2003). If the government spends 100 dollars and taxes 100 dollars (balanced budget) then private accumulation of fiat currency (savings) is zero in that period and the private budget is balanced. Say the government spends 120 and taxes remain at 100, then private saving is 20 dollars which can accumulate as financial assets (in this case, 20 dollar notes although to encourage saving the government may decide to issue an interest-bearing bond). The government deficit of 20 is exactly the private savings of 20. Now if government continued in this vein, accumulated private savings would equal the cumulative budget deficits. However, should government decide to run a surplus (say spend 80 and tax 100) then the private sector would owe the government a net tax payment of 20 dollars. The government may agree to buy back some bonds it had previously sold. Either way accumulated private saving is reduced dollar-for-dollar when there is a government surplus. The government surplus has two negative effects for the private sector: (a) the stock of financial assets (money or bonds) held by the private sector, which represents its wealth, falls; and (b) private disposable income also falls in line with the net taxation impost. Some may retort that government bond purchases provide the private wealth-holder with cash. That is true but the liquidation of wealth is driven by the shortage of cash in the private sector arising from tax demands exceeding income. The cash from the bond sales pays the Government's net tax bill. The result is exactly the same when expanding this example by allowing for private income generation and a banking sector.

Figure 1 Government and Non-Government structure

�

From the example above, and further recognising that currency plus reserves (the monetary base) plus outstanding government securities constitutes net financial assets of the non government sector, the fact that the non-government sector is dependent on the government to provide funds for both its desired net savings and payment of taxes to the government becomes a matter of accounting.

Macroeconomics textbooks use a 'sectoral flows' framework to summarise the accounting of income flows between the government, private and foreign sectors. With a consolidated private sector including the foreign sector, total private savings has to equal private investment plus the government budget deficit. If we disaggregate the non-government sector into the private and foreign sectors, then total private savings is equal to private investment, the government budget deficit, and net exports, as net exports represent the net financial asset savings of non residents. If the aim was to boost the savings of the private domestic sector, when net exports are in deficit, then as Wray (1998: 81) suggests �taxes in aggregate will have to be less than total government spending."

This framework also allows us to see why the pursuit of government budget surpluses will be contractionary. Pursuing budget surpluses is necessarily equivalent to the pursuit of non-government sector deficits. They are two sides of the same coin. The decreasing levels of net savings 'financing' the government surplus increasingly leverage the private sector and the deteriorating debt to income ratios will eventually see the system succumb to ongoing demand-draining fiscal drag through a slow-down in real activity.

So the macroeconomic principles that emerge from this discussion are:

1.�Budget surpluses reduce private savings (increase private debt);

2.�Budget surpluses do not add to government wealth or their ability to spend;

3.�Budget surpluses can be achieved only through decreases in non-government savings (increases in non-government debt);

4.�Budget surpluses reduce aggregate demand;

5.�Governments run surpluses in order to reduce private savings and reduce consumer demand;

6.�Alternatively governments run deficits to increase private savings and increase private demand; and

7.�The concept of government needing 'finance' before they can spend is never an issue.

�

2.2�Government spending is not revenue constrained

Government spending is not inherently revenue constrained. Unlike the government of issue, a private citizen is constrained by the sources of available funds, including income from all sources, asset sales and borrowings from external parties. Federal government spending, however, is facilitated in the main, by the government issuing cheques drawn on the central bank. The arrangements the government has with its central bank to account for this are largely irrelevant. When the recipients of the cheques (sellers of goods and services to the Government) deposit the cheques in their bank, they clear through the central banks clearing balances (reserves), and credit entries appears in accounts throughout the commercial banking system. In other words, government spends simply by crediting a private sector bank account at the central bank. Operationally, this process is independent of any prior revenue, including taxing and borrowing. Nor does the said 'account crediting' in any way reduce or otherwise diminish any government asset or government's ability to further spend.

Alternatively, when taxation is paid by the private sector cheques (or bank transfers) that are drawn on private accounts in the member banks, the central bank debits a private sector bank account. No real resources are transferred to government. Nor is government's ability to spend augmented by said debiting of private bank accounts.

In general, mainstream economics errs by blurring the differences between private household budgets and the government budget. This errant analogy is advanced by the popular government budget constraint framework (GBC) that now occupies a chapter in any standard macroeconomics textbook.� The GBC is used by orthodox economists to analyse three alleged forms of public 'finance': (1) Raising taxes; (2) Selling interest-bearing government debt to the private sector (bonds); and (3) Issuing non-interest bearing high powered money (money creation). Various scenarios are constructed to show that either deficits are inflationary, if financed by high-powered money (debt monetisation), or squeeze private sector spending, if financed by debt issue. While in reality the GBC is just an ex post accounting identity, orthodox economics claims it to be an ex ante financial constraint on government spending.

The GBC leads students to believe that unless the government wants to 'print money' and cause inflation it has to raise taxes or sell bonds to get 'money' in order to spend. Bell (2000: 617) says that the erroneous understanding that a student will gain from a typical macroeconomics course is that �the role of taxation and bond sales is to transfer financial resources from households and businesses (as if transferring actual dollar bills or coins) to the government, where they are respent (i.e., in some sense 'used' to finance government spending)."

What is missing is the recognition that a household, the user of the currency, must finance its spending, ex ante, whereas government, the issuer of the currency, necessarily must spend first (credit private bank accounts) before it can subsequently debit private accounts, should it so desire. The government is the source of the funds the private sector requires to pay its taxes and to net save (including the need to maintain transaction balances), making government solvency in its currency of issue a given and a non issue.

Standard macro textbooks struggle to explain this to students. Usually, there is some text on 'money creation' but no specific discussion of the accounting that underpins spending, taxation and debt-issuance. Blanchard (1997: 429) is representative and says government �can also do something that neither you nor I can do. It can, in effect, finance the deficit by creating money. The reason for using the phrase 'in effect,' is that � governments do not create money; the central bank does. But with the central bank's cooperation, the government can in effect finance itself by money creation. It can issue bonds and ask the central bank to buy them. The central bank then pays the government with money it creates, and the government in turn uses that money to finance the deficit. This process is called debt monetization."

However, this conception has no application. The subject of debt monetisation frequently enters discussions of monetary policy in economic text books and the broader public debate. Following Blanchard's conception, debt monetisation is usually referred to as a process whereby the central bank buys government bonds directly from the treasury. In other words, the federal government borrows money from the central bank rather than the public. Debt monetisation is the process usually implied when a government is said to be printing money. Debt monetisation, all else equal, is said to increase the money supply and can lead to severe inflation. However, fear of debt monetisation is unfounded, not only because the government doesn't need money in order to spend but also because the central bank does not have the option to monetise any of the outstanding federal debt or newly issued federal debt.

As long as the central bank has a mandate to maintain a target short-term interest rate, the size of its purchases and sales of government debt are not discretionary. Once the central bank sets a short-term interest rate target, its portfolio of government securities changes only because of the transactions that are required to support the target interest rate (see Section 2.5). The central bank's lack of control over the quantity of reserves underscores the impossibility of debt monetisation. The central bank is unable to monetise the federal debt by purchasing government securities at will because to do so would cause the funds rate to fall to zero (or the 'support rate'). If the central bank purchased securities directly from the treasury and the treasury then spent the money, its expenditures would be excess reserves in the banking system. The central bank would be forced to sell an equal amount of securities to support the target interest rate. The central bank would act only as an intermediary. The central bank would be buying securities from the treasury and selling them to the public. No monetisation would occur.

To monetise means to convert to money. Gold used to be monetised when the government issued new gold certificates to purchase gold. In a broad sense, federal debt is money, and deficit spending is the process of monetising whatever the government purchases. Monetising does occur when the central bank buys foreign currency. �Purchasing foreign currency converts, or monetises, that currency to dollars. The central bank then offers federal government securities for sale to offer the new dollars just added to the banking system a place to earn interest. This often misunderstood process is referred to as sterilisation. As Wray (1998: ix) notes �in reality, all government spending is 'financed' by 'money creation', but this money is accepted because there is an enforced tax liability that is, by design, burdensome."

The fundamental macroeconomic principles that emerge from this Section are:

1. Governments spend (introduce net financial assets into the economy) by crediting bank accounts in addition to issuing cheques or tendering cash.

2.�This spending is not 'revenue constrained'. A currency-issuing government has no financial constraints on its spending, which is not the same thing as acknowledging self imposed (political) constraints.

�

2.2�Vertical and horizontal relationships in a modern monetary economy

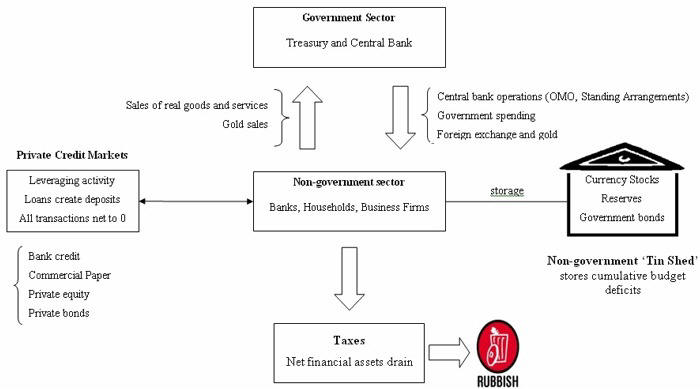

In Figure 1, we depicted a vertical relationship between the government and non-government sectors. What are these vertical transactions between the government and non-government sectors and what is the importance of them for understanding how the economy works? In the previous sections we characterised them as being injections/withdrawals of net financial assets. In Figure 2, the juxtaposition between vertical and horizontal relationships in the economy is shown as the basis for the following discussion. Arrows going down depict vertical transactions between the government and non-government sectors and horizontal arrows depict transactions between agents within the non-government sector.

In terms of the vertical relationships, Mosler and Forstater (1998) say that �The tax liability lies at the bottom of the vertical, exogenous, component of the currency. At the top is the State (here presented as a consolidated Treasury and Central Bank), which is effectively the sole issuer of units of its currency, as it controls the issue of currency units by any of its designated agents. The middle is occupied by the private sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates what is left over (State deficit spending) in the form of cash in circulation, reserves (clearing balances at the State's Central Bank), or Treasury securities (deposits; offered by the CB) � The currency units used for the payment of taxes (or any other currency units transferred to the State), for this analysis, is considered to be consumed (destroyed) in the process. As the State can issue paper currency units or accounting information at the CB at will, tax payments need not be considered a reflux back to the state for the process to continue."

The two arms of government (treasury and central bank) have an impact on the stock of accumulated financial assets in the non-government sector and the composition of the assets. The government deficit (Treasury operation) determines the cumulative stock of financial assets in the private sector. Central bank decisions then determine the composition of this stock in terms of notes and coins (cash), bank reserves (clearing balances) and government bonds.

Why are taxes at the bottom of the 'exogenous vertical chain' and go to 'rubbish'? Building on the insights from the previous section, we can articulate more macroeconomic principles that provide an answer to this question:

1.�Taxes reduce balances in private sector bank accounts.

2.�The Government doesn't actually 'get anything' � the reductions are accounted for but 'go nowhere'.

3. The concept of a fiat-issuing Government 'saving' in its own currency is of no relevance. Governments may use its net spending to purchase stored assets ('spending the surpluses' on gold!) but that is not the same as saying when governments run surpluses (taxes in excess of spending) the funds are stored and can be 'spent' in the future. This concept is erroneous.

4.�Payments for bond sales are also accounted for as a drain on liquidity but then also scrapped (see section 2.5).

The private credit markets represent relationships (depicted by horizontal arrows) and 'house' the leveraging of credit activity by commercial banks, business firms, and households (including foreigners), which Post Keynesians consider to be endogenous circuits of money. The crucial distinction is that the horizontal transactions do not create net financial assets � all assets created are matched by a liability of equivalent magnitude so all transactions net to zero. The implications of this are dealt with in Section 2.6 when we consider the impacts of net government spending on liquidity and the role of bond issuance.

Figure 2 also shows what we term the 'Non-government Tin Shed' which stores fiat currency stocks, bank reserves and government bonds. Following our earlier discussion, any payment flows from the Government sector to the Non-government sector that do not 'finance' the taxation liabilities remain in the Non-government sector as cash, reserves or bonds. So we can understand any stocks in the 'Tin Shed' as being the reflection of the cumulative budget deficits.

The other important point is that private leveraging activity, which nets to zero, are not an 'operative' part of the 'Tin Shed' stores of currency, reserves or government bonds. The commercial banks do not need reserves to generate credit, contrary to the popular representation in standard textbooks. We learn more about this in Section 2.5.

�Figure 2 Vertical and horizontal macroeconomic relations

�2.3 State money introduces the possibility of unemployment

Once we realise that government spending is not revenue-constrained then we have to analyse the functions of taxation in a different light. The starting point of this new understanding is that taxation functions to promote offers from private individuals to government of goods and services in return for the necessary funds to extinguish the tax liabilities.

In this way, it is clear that the imposition of taxes creates unemployment (people seeking paid work) in the non-government sector and allows a transfer of real goods and services from the non-government to the government sector, which in turn, facilitates the government's economic and social program.

The crucial point is that the funds necessary to pay the tax liabilities are provided to the non-government sector by government spending. Accordingly, government spending provides the paid work which eliminates the unemployment created by the taxes.

So it is now possible to see why mass unemployment arises. It is the introduction of 'State Money' (government taxing and spending) into a non-monetary economics that raises the spectre of involuntary unemployment. As a matter of accounting, for aggregate output to be sold, total spending must equal total income (whether actual income generated in production is fully spent or not each period). Involuntary unemployment is idle labour offered for sale with no buyers at current prices (wages). Unemployment occurs when the private sector, in aggregate, desires to earn the monetary unit of account, but doesn't desire to spend all it earns, other things equal. As a result, involuntary inventory accumulation among sellers of goods and services translates into decreased output and employment. In this situation, nominal (or real) wage cuts per se do not clear the labour market, unless those cuts somehow eliminate the private sector desire to net save, and thereby increase spending.

2.4 Unemployment occurs when net government spending is too low

The purpose of State Money is for the government to move real resources from private to public domain. It does so by first levying a tax, which creates a notional demand for its currency of issue. To obtain funds needed to pay taxes and net save, non-government agents offer real goods and services for sale in exchange for the needed units of the currency. This includes, of-course, the offer of labour by the unemployed. The obvious conclusion is that unemployment occurs when net government spending is too low to accommodate the need to pay taxes and the desire to net save.

This analysis also sets the limits on government spending. It is clear that government spending has to be sufficient to allow taxes to be paid. In addition, net government spending is required to meet the private desire to save (accumulate net financial assets). From the previous paragraph it is also clear that if the Government doesn't spend enough to cover taxes and desire to save the manifestation of this deficiency will be unemployment. Keynesians have used the term demand-deficient unemployment. In our conception, the basis of this deficiency is at all times inadequate net government spending, given the private spending decisions in force at any particular time.

For a time, inadequate levels of net government spending can continue without rising unemployment. In these situations, as is evidenced in Australia over the last several years GDP growth can be driven by an expansion in private debt. The problem with this strategy is that when the debt service levels reach some 'threshold' percentage of income, the private sector will attempt to restructure their balance sheets to make them less precarious and as a consequence the demand for debt slows and the economy falters. In this case, any fiscal drag (inadequate levels of net spending) begins to manifest as unemployment.

The point is that for a given tax structure, if people want to work but do not want to continue consuming (and going further into debt) at the previous rate, then the Government can increase spending and purchase goods and services and full employment is maintained. The alternative is unemployment and a recessed economy.

2.5 The central bank administers the risk free interest rate and Government debt functions to support it

The central bank necessarily administers the risk-free interest rate and is not subject to direct market forces. The orthodox macroeconomic approach argues that persistent deficits �reduce national savings � [and require] � higher real interest rates and lower levels of investment spending" (DeLong, 2002:405). Unfortunately, proponents of this logic which automatically links budget deficits to increasing debt issuance and hence rising interest rates fail to understand how interest rates are set and the role that debt issuance plays in the economy. At the outset, the interest rate is set by the central bank which can choose to leave it at 0, regardless.

While the funds that government spends do not 'come from' anywhere and taxes collected do not 'go anywhere' (Mitchell and Mosler, 2002), there are substantial liquidity impacts from net government positions as discussed. If the funds that purchase the bonds come from government spending as the accounting dictates then any notion that government spending rations finite 'savings' that could be used for private investment is a nonsense. Nugent (2003) says �One can also see that the fears of rising interest rates in the face of rising budget deficits make little sense when all of the impact of government deficit spending is taken into account, since the supply of treasury securities offered by the federal government is always equal to the newly created funds. The net effect is always a wash, and the interest rate is always that which the Fed votes on. Note that in Japan, with the highest public debt ever recorded, and repeated downgrades, the Japanese government issues treasury bills at .0001%! If deficits really caused high interest rates, Japan would have shut down long ago!"

To understand why budget deficits operationally place downward pressure on short-term interest rates, we note that net government spending (deficits) will eventually, presuming the increased private demand for cash is less than the injection, manifest as excess reserves (cash supplies) in the clearing balances (bank reserves) of the commercial banks at the central bank. As noted in Section 2.2, exchanges between clearing accounts are horizontal transactions and in settlement sum to zero in terms of the system-wide balance. Thus, in net terms the money market cash position is unchanged.

As explained earlier, only transactions between the federal government and the private sector change the system balance. Government spending and purchases of government securities (treasury bonds) by the central bank add liquidity and taxation and sales of government securities drain liquidity. These transactions influence the cash position of the system on a daily basis and on any one day they can result in a system surplus (deficit) due to the outflow of funds from the official sector being above (below) the funds inflow to the official sector. The system cash position has crucial implications for central bank monetary policy, which targets the level of short-term interest rates. The system balance is an important determinant of the use of open market operations (bond purchases and sales) by the central bank.

How the central bank manages the so-called 'spread', the difference between the rate that the central bank pays on reserve balances and the short-term interest rate (the 'operational target rate'), influences the range in which the short-term interest rate can fluctuate. Many countries (such as Canada, Australia) maintain a default return on surplus reserve account (for example, the Reserve Bank of Australia pays a default return equal to 25 basis points less than the overnight cash rate on surplus Exchange Settlement accounts). This effectively creates a 'corridor' within which the short-term interest rates can fluctuate with liquidity variability. Other countries like the US and Japan do not offer a return on reserves which means persistent excess liquidity will drive the short-term interest rate to zero (as in Japan) if the government does not sell bonds (or raise taxes).

What impact does a budget deficit have on the system-wide liquidity? Fiscal deficits result in system-wide surpluses, after spending and portfolio adjustment has occurred. The commercial banks will be faced with earning the lower default return on surplus reserve funds which will put downward pressure on the cash rate. If the central bank desires to maintain the current target cash rate then it must 'drain' this surplus liquidity by selling government debt.

This allows us to understand the role of government debt issuance. Government debt functions as interest rate support and not as a source of funds. Once we understand the actual process of government spending, described above, which recognises the fiscal policy influence on bank reserves, we can more fully appreciate the role debt-issuance plays. Once again, mainstream textbooks are totally misleading. Blanchard (1997: 429) cautions against what he erroneously calls debt monetisation and instead claims that �most of the time and in most countries, deficits are financed primarily through borrowing rather than through money creation." He says that borrowing is facilitated by issuing bonds. But a moment's reflection will reveal that this description has no application in a modern fiat currency economy.

Returning to the discussion about bank reserves and drawing on our earlier two-person economy, in an accounting sense the 'money' that is used to buy bonds (that is regarded as 'financing government spending') is the same 'money' (in aggregate) that the government spent. Nugent (2003) says that �in other words, deficit spending creates the new funds to buy the newly issued securities." To use the language of central bankers, government securities function to 'offset operating factors that add reserves', the largest 'operating factor' being net spending by the Treasury. In this sense, the purchase (or sale) of bonds by (to) the non-government sector alter the distribution of the assets in the 'Tin Shed' shown in Figure 2.

Therefore, it is clear that government debt does not finance spending but rather serves to maintain reserves such that a particular cash rate can be defended by the central bank. What would happen if the government sold no securities? The 'penalty' for the government that doesn't pay interest on reserves would be a Japan-like zero interest rate, rather than the positive cash rate target. For the central bank running a default support rate, the 'penalty' would be that the interest rate would fall to its support rate. Importantly, any economic ramifications (like inflation or currency depreciation) would be due to the lower interest rate rather than any notion of monetisation..

Accordingly, the concept of 'debt monetisation' is a non sequitur. Once the cash rate target is set, the central bank should only trade government securities if liquidity changes are required to support this target. Given the central bank cannot really control the reserves then debt monetisation is strictly impossible. Imagine that the central bank traded government securities with the treasury, which then increased government spending. The excess reserves would force the central bank to sell the same amount of government securities to the private market or allow the cash rate to fall to the support level. This is not 'monetisation' but rather the central bank simply acting as 'broker' in the context of the logic of the interest rate setting monetary policy.

Ultimately, private agents may refuse to hold any more cash or bonds. With no debt issues, the interest rates will fall to the central bank support limit (which may be zero). It is then also clear that the private sector at the micro level can only dispense with unwanted cash balances in the absence of government paper by increasing their consumption levels. Given the current tax structure, this reduced desire to net save would generate a private expansion and reduce the deficit, eventually restoring the portfolio balance at higher private employment levels and lower the required budget deficit as long as savings desires remain low. Clearly, there would be no desire for the government to expand the economy beyond its real limit. Whether this generates inflation depends on the ability of the economy to expand real output to meet rising nominal demand. That is not compromised by the size of the budget deficit.

The fundamental principle established in this Section is:

1.��The central bank sets the short-term interest rate based on its policy aspirations;

2.�Government spending is independent of borrowing which the latter best thought of as coming after spending;

3.��Budget deficits put downward pressure on interest rates contrary to the myths that appear in macroeconomic textbooks about 'crowding out';

4.��The 'penalty for not borrowing' is that the interest rate will fall to the bottom of the 'corridor' prevailing in the country which may be zero if the central bank does not offer a return on reserves, For example Japan easily maintains a zero interest rate policy with record budget deficits simply by spending more than it borrows.

5.��Government debt-issuance is a 'monetary policy' consideration rather than being intrinsic to 'fiscal policy', although in a modern monetary paradigm the distinctions between monetary and fiscal policy as traditionally defined are moot.

6.��The traditional notion of 'debt monetisation' is not applicable (see also Section 2.2).

7.��A budget surplus describes what the government 'had done' not what it 'has received'.

�

3.�The US social security privatisation debate

In answer to the question 'Why does Social Security need reform?', the conservative US think tank, the Cato Institute (2005) says that �Social Security is going bankrupt. The federal government's largest spending program, accounting for nearly 22 percent of all federal spending, faces irresistible demographic and fiscal pressures that threaten the future retirement security of today's young workers. According to the 2003 report of the Social Security system's Board of Trustees, in 2018, just 14 years from now, the Social Security system will begin to run a deficit. That is, it will begin to spend more on benefits than it brings in through taxes. Anyone who has ever run a business - or balanced a checkbook - understands that when you are spending more than you bring in, something has to give - you need to start either earning more money or spending less to keep things balanced. For Social Security, that means either higher taxes or lower benefits."

Other public commentators, opposed to government deficits also use the 'household' analogy to analyse government � the classic fallacy underpinning the GBC literature as noted in Section 2.2. In relation to the so-called 'unfunded obligations' on the US government for their social programs like Medicare, Social Security, Medicaid, federal employee pensions, Gokhale and Smetters (2003) wrote �To understand the problem, suppose your 18-year-old kid moved out of your house last month and got a job to cover his rent. He made $2,000 in the month and paid $1,000 in rent. Food and utilities cost another $800. On a cash flow basis, everything appears great. He has $200 left over to put into the bank. But your opinion of his financial position would change if you also discovered that he had built up another $500 in credit card charges during his first month and that he planned on doing so every month into the future. You would wisely inform him that he was actually $300 in the red and that he should quickly change his spending habits � Unfortunately, the budgeting by the U.S. federal government does not take into account the growing 'credit card' debt that is being created by the nation's large entitlement programmes."

The fallacy in reasoning is simple for a person well-trained in modern macroeconomics to pick. The '18 year old kid' is a user of the currency whereas the US federal government is the issuer of the currency. This difference is crucial because the issuer has a totally different set of long-term options open to them than the user, who has to obey their budget constraint. The issuer has no financial constraint on their spending. This sort of fallacy pervades the social security debate in the US.

The US President's plan is to privatise social security in the US by creating individual retirement accounts. The plan, announced in the State of the Union speech, will mean that a portion of the payroll tax contributions paid by workers and firms which currently notionally form the 'fund' that purchases the bonds for the trust fund will now be used to finance the individual investment accounts. Then each worker will choose how they will invest these funds across a variety of investment options each of which will vary in risk and return. The claim is that these funds will eliminate the 'fiscal burden' of providing pensions for retirees and ensure the system does not become 'bankrupt'.

The critics of the plan are often equally misguided. They argue 'as if' social security can become bankrupt. In this light they vigorously work out ways it can raise more revenue or reduce outlays. They deny the existence of an 'immediate crisis', pointing out that the security trust fund has an accumulated reserve of $1.5 trillion which is held in the form of government bonds. They say that any (alleged) long-run financial gaps are less than the planned (cumulative) tax cuts proposed by the current regime. They indicate that taxes could slowly rise to 'finance' any short-falls. Finally, (as a broad representation of the criticisms), they claim that indexing against price deflation could replace the current linking of pensions to real wage increases to make it 'more affordable'.

Notable 'progressive economists' even fall foul in relation to the alleged bankruptcy issue, Baker (2004) says �One such claim that gets frequently repeated is that the Social Security trust fund has been 'raided', 'spent', or is just worthless pieces of paper. In fact, the Social Security trust fund holds almost $2 trillion of government bonds. Under the law, the government must repay these bonds to Social Security from general revenue - this means it will be repaid primarily from progressive personal and corporate income taxes, because workers have already paid for their Social Security benefits. In other words, the government is obligated to tax wealthy people like Donald Trump and Peter Peterson (the founder of the Concord Coalition) to pay for the Social Security benefits that the rest of us have already earned ... The Social Security system lent money to the government to buy these bonds. (This is by design - the trust fund was built up to help pay for the retirement of the baby boomers). The fact that the government spent the money is meaningless - just as it is meaningless if the government spends the money it borrows by issuing any other bond. The government is still legally obligated to repay the bond. In short, the people who say 'there is no trust fund' are misleading the public. There is a trust fund with $2 trillion (growing at the rate of $200 billion a year) unless we let Congress eliminate it."

All these claims are erroneous and provide no basis for arguing against the privatisation at its root cause - the fallacy that there is a government budget constraint. As we have seen in Section 2, net government spending underpins the ability of the private sector to pay taxes and to save. The vital point is that the government will always be able to spend the required fiat to provide social security payments for its elderly population. The only 'costs' of keeping old people alive are the 'real resources' they consume. Whether the spending required to purchase these resources comes from private or public means is of no particular import to deciding whether a nation can 'afford' these real resources. If they are available, then public spending can always purchase them without any consideration of 'raising revenue'.

IF GOVT FINANCE WERE CORRECTLY UNDERSTOOD, AT BEST THE FINANCIAL ARGUMENT WOULD CONCERN THE POSSIBLE 'INFLATION' OUTCOME OF TODAY'S FISCAL STRUCTURE.� INSTEAD OF ARGUING INSOLVENCY, FOR EXAMPLE, THE ADMINISTRATION MIGHT ARGUE ABOUT THE FUTURE LEVEL OF 'INFLATION.'� THE FACT THAT NO ONE HAS EVEN BEGUN SUCH A CALCULATION IS FURTHER EVIDENCE OF A TOTAL FAILURE TO GRASP THE ACTUAL ISSUE.

So what is the real issue? The debate about whether social security should be private or publicly-provided is not an economic one. It is am outcome of political choice. We can easily provide a public scheme without it ever becoming bankrupt. The concept of bankruptcy has no application to a government which is the monopoly provider of the fiat currency. As the demands of the aged for health care and whatever increases it becomes a political choice mediated through the electoral process as to how far public spending accommodates these demands. It requires that we convert primary schools into aged care facilities and similar demographically motivated shifts in the emphasis of public spending as our population ages. We might decide as a nation not to do this. We might decide that we will not provide satisfactory public services for the aged members of our population. But there will never be a financial (government budget) reason for not doing this - only the political choice.

�

4.�The intergenerational myth in Australia

The proposed privatisation of the US social security system is just another example of how the economic debate operates in the wrong paradigm - that of a government budget constraint. It shares the same erroneous analysis that impoverishes the Australian government's claims about the intergenerational debate and the need to run 'budget surpluses now' to 'save for the future'. The Intergenerational Report (IGR) (2002: 1) begins by saying that �Commonwealth government finances are � [presently] � strong."

From Section 2 it is clear that Federal finances can be neither strong nor weak but in fact merely reflect a �scorekeeping" role. We have learnt that when Government boasts that a $7.2 billion surplus in 2002-03, this is tantamount to saying that non-government $A financial asset savings recorded a decline of $7.2 billion over the same period. Thus the IGR (2002: 1) claim that the �The Commonwealth Budget recorded an accumulated cash surplus of $23.7 billion from 1997-98 to 2000-01" is equivalent to saying that non-government $A financial asset savings declined by $23.7 billion over the same period.

Equally, the IRG (2002: 1) claim that �During this period, Commonwealth government net debt, already one of the lowest among the industrialised economies, has fallen from $82.9 billion to $39.3 billion" is equivalent to saying that non-government holdings of government debt fell by the same amount over this period. In other words, private sector wealth was destroyed in order to generate the funds withdrawal that is accounted for as the surplus.

The IRG (2002: 1) claims this accounting record is achieved through �sound fiscal management � [and] � has provided the platform for vigorous, low inflationary growth � generating jobs and higher incomes for Australians." Once we appreciate the equivalents noted above we would conclude that this draining of financial equity introduces a deflationary bias that has slowed output and employment growth (keeping unemployment at unnecessarily high levels) and has forced the non-government sector into relying on increasing debt to sustain consumption.

These insights help us understand the errors in the logic underpinning the IGR and the issue in general. Financial commentators often suggest that budget surpluses in some way are equivalent to accumulation funds that a private citizen might enjoy. The resonance with the US debate in relation to their Social Security Trust Fund is manifest (Eisner, 1998; Penner et al, 1999; Bell and Wray, 2000). Our conclusions concerning the IGF proposal mirror the arguments raised against the logic used in the US context. This idea that accumulated surpluses allegedly 'stored away' will help government deal with increased public expenditure demands that may accompany the ageing population lies at the heart of the IGR misconception. While it is moot that an ageing population will place disproportionate pressures on government expenditure in the future (Kinnaird, 2002), we would argue that the concept of pressure is inapplicable because it assumes a financial constraint. We have already shown this assumption is erroneous.

The IGR (2002: 1) considers that �taxpayers' funds" will be squeezed. But the notion that taxpayers fund 'anything' is erroneous. As we have seen, taxes are paid by debiting accounts of the member commercial banks accounts whereas spending occurs by crediting the same. The notion that 'debited funds' have some further use is not applicable. When taxes are levied the revenue does not go anywhere. The flow of funds is accounted for, but accounting for a surplus that is merely a discretionary net contraction of private liquidity by government does not change the capacity of government to inject future liquidity at any time it chooses (Mitchell and Mosler, 2002).

The standard GBC intertemporal analysis that deficits lead to future tax burdens is also problematic. The IGR (2002: 1) falls into this error claiming that �if policies are not adjusted, the current generation of taxpayers is likely to impose a higher tax burden on the next generation." The problem is that the GBC is not a 'bridge' that spans the generations in some restrictive manner. Each generation is free to select the tax burden it endures. Taxing and spending transfers real resources from the private to the public domain. Each generation is free to select how much they want to transfer via political decisions mediated through political processes. For example, if the world builds 100 million cars in 2040 will it have to send them back in time to 'pay off' the debt? Of-course not, those cars will be driven then, presumably by the living.

When we argue that there is no financial constraint on federal government spending we are not, as if often erroneously claimed, saying that government should therefore not be concerned with the size of its deficit. We are not advocating unlimited deficits. Rather, the size of the deficit (surplus) will be market-determined by the desired net saving of the non-government sector. This may not coincide with full employment and so it is the responsibility of the government to ensure that its taxation/spending are at the right level to ensure that this equality occurs at full employment. Accordingly, if the goals of the economy are full employment with price level stability then the task is to �ensure that government spending is at just the right level so that neither inflationary nor deflationary forces are induced" (Wray, 1998: ix).

This insight puts the idea of sustainability of government finances into a different light. The IGR (2002: 1) logic is that forward planning is necessary �to ensure that governments will be well placed to meet emerging policy challenges in a timely and effective manner." What we know is that if the Federal government continues to run budget surpluses to keep Commonwealth debt low then it will ensure that further deterioration in non-government savings will occur until aggregate demand decreases sufficiently to slow the economy down and raise the output gap.

We agree that the goal should be to maintain an �efficient and effective medical health system" (IGR, 2002: 1). Clearly the real health care system matters by which we mean the resources that are employed to deliver the health care services and the research that is done by universities and elsewhere to improve our future health prospects. So real facilities and real know how define the essence of an effective health care system.

Clearly maximising employment and output in each period is a necessary condition for long-term growth. The emphasis in the IGR (2002: 2) on �encouraging mature age participation in the labour force" is clearly desirable and contrary to current government policy which reduces job opportunities for older male workers (Mitchell and Carlson, 2001). We can agree that anything that has a positive impact on the dependency ratio is desirable and the best thing for that is ensuring that there is a job available for all those who desire to work.

But this is about political choices rather than government finances. To summarise our argument, the ability of government to provide necessary goods and services to the non-government sector, in particular, those goods that the private sector may under-provide is independent of government finance. Any attempt to link the two via fiscal policy 'discipline', will not increase per capita GDP growth in the longer term. The reality is that fiscal drag that accompanies such 'discipline' reduces growth in aggregate demand and private disposable incomes, which can be measured by the foregone output that results. Clearly fiscal discipline �helps maintain low inflation" (IGR, 2002: 2) because it acts as a deflationary force relying on sustained excess capacity and unemployment to keep prices under control. Fiscal discipline is also claimed to increase national savings. But this is a construct of economic consequence only under fixed exchange rate regimes and is not applicable to floating exchange rate regimes. Further we have shown in Section 2 that budget surpluses are dollar-for-dollar reductions in non-government savings, the latter being the relevant measure of how well the private sector can provide for themselves in the future..

�

4.�Conclusion � the solution is full employment

This paper has made three major points. First, the idea that it is necessary for the Federal government to stockpile financial resources to ensure it can provide services required for an ageing population in the years to come has no application. It is not only invalid to construct the problem as one being the subject of a financial constraint but even if such a stockpile was successfully stored away in a vault somewhere there would be still no guarantee that there would be available real resources in the future (see Foster, 1981, Wray, 1999). Discussions about 'war chests' completely misunderstand the options available to the Federal government in a fiat currency economy. Second, the best thing to do now is to maximise incomes in the economy by ensuring there is full employment. This requires a vastly different approach to fiscal and monetary policy than is currently being practised. Third, if there are sufficient real resources available in the future then their distribution between competing needs will become a political decision which economists have little to add.

Long-run economic growth that is also environmentally sustainable will be the single most important determinant of sustaining real goods and services for the population in the future. Principal determinants of long-term growth include the quality and quantity of capital (which increases productivity and allows for higher incomes to be paid) that workers operate with. Strong investment underpins capital formation and depends on the amount of real GDP that is privately saved and ploughed back into infrastructure and capital equipment. Public investment is very significant in establishing complementary infrastructure upon with private investment can deliver returns. A policy environment that stimulates high levels of real capital formation in both the public and private sectors will engender strong economic growth.

4.1�A final irony

A current mainstream belief is that for all practical purposes there is no real investment that can be made today that will remain useful 50 years from now apart from education, in the hope that when the time comes we will best be able to deal with whatever real problems arise. Unfortunately, they choose to address the problems of the distant future as monetary problems, and conclude that we need 'austerity' today to prepare us for the future. And, both ironically, and as evidence of the lack of understanding of the real problems we could be addressing, public education is universally one of the first expenditures that are reduced.

�

References

Baker, D. (2004) 'Cutting our benefits', In the Times, December 6, available at http://www.inthesetimes.com/site/main/article/1738/.

Bell, S. (2000) 'Do Taxes and Bonds Finance Government Spending?', Journal of Economic Issues, 34, 603-620.

Bell, S. and Wray, L.R. (2000) 'Financial Aspects of the Social Security �Problem"', Working Paper No. 5, Center for Full Employment and Price Stability, available at http://www.cfeps.org/pubs/wp/wp5.

Blanchard, O. (1997) Macroeconomics, Upper Saddle River, Prentice-Hall.

Cato Institute (2005) Why does Social Security need reform?, available at http://www.socialsecurity.org.

Commonwealth Treasury (IGR) (2002) Intergenerational Report 2002-03, Budget Paper No. 5, May 14, Commonwealth of Australia.

Delong, J.B. (2002) Macroeconomics, McGraw-Hill, Sydney.

Eisner, R. (1998) 'Save Social Security from its Saviors', Journal of Post Keynesian Economics, 21(1), 77-92.

Foster, J. (1981) 'The Reality of the Present and the Challenge of the Future', Journal of Economic Issues, 15(4), 963-968.

Gokhale, J. and Smetters, K. (2003) 'America's budget book-keeping scandal', Financial Times, September 9, 2003.

Kinnear, P. (2002) 'Ageing - will the real culprit please stand up?', June, available at http://www.onlineopinion.com.au/2002/Jun02/Kinnear.htm.

Mitchell, W.F. and Carlson, E. (2001) Unemployment: the tip of the iceberg, Sydney, CAER/UNSW Press.

Mitchell, W.F. and Mosler, W.B. (2002) 'Fiscal policy and the Job Guarantee', Australian Journal of Labour Economics, 5(2), 243-60.

Mosler, W.B. (1995) Soft Currency Economics, http://www.mosler.org/docs/docs/soft0004.htm

Mosler, W. and Forstater, M. (1998) A General Analytical Framework for the

Analysis of Currencies and Other Commodities, (available at http://www.warrenmosler.com).Nugent, T.E. (2003) 'The Budget Deficit/The Budget Surplus: The Real Story', available at http://www.mosler.org/docs/docs/budget_deficit_real_story.htm.

Penner, R., Solanki, S., Toder, E. and Weisner, M. (1999) 'Saving the Surplus to Save Social Security: What Does it Mean?', Brief Series, No. 7, Urban Institute, October, http://www.urban.org/retirement.

State of Union (2005), http://www.whitehouse.gov/stateoftheunion/2005/index.html.

Wray, L.R. (1998) Understanding Modern Money: The Key to Full Employment and Price Stability, Cheltenham, Edward Elgar.

Wray, L.R. (1999) 'The Emperor Has No Clothes: President Clinton's Proposed Social Security Reform', Public Policy Note, No. 2, Jerome Levy Economics Institute.

[1] The authors are Professor of Economics and Director of the Centre of Full Employment and Equity, and Distinguished Research Fellow, Centre of Full Employment and Equity and Principal, III Offshore Advisors, St. Croix, respectively.